Stock Market Scaling

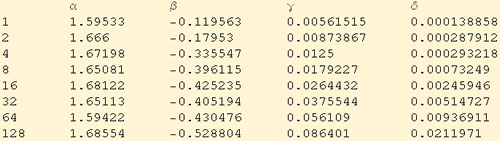

Mandelbrot described scaling behavior for cotton prices. That same scaling behavior is present in the LogReturns of the Dow Jones Industrial series. Independently identically distributed stable sequences of random variables will scale when summed with the property that a and ß remain constant. For the S(α, ß, γ, δ; 1) parameterization

![]()

The data are partitioned into intervals according to powers of two, then each partition is summed; the resulting data sequence is fit to stable parameters. The periods cover time intervals of one trading day to 128 trading days or about six months. If one tries longer intervals, sample sizes become too small for reliable fitting.

There is a clear linear relationship in the log-log plot of Log[γ] versus interval. The scaling for the calculated values of delta is a little less perfect.

![]()